The What and When of Angel Returns

Show me the Money!

The first thing everyone asks when they start with Angel is, “How much money can I make.” We’ve all heard about the angels who invested $25K in the Uber seed round and 9 years later walked away with $125M after the IPO. Obviously, Uber doesn’t happen every day.

How do you make money when most startups fail?

It’s called the power law.

The graph below reflects the type of returns you’ll see in a diverse startup portfolio.

50% of your investments will go to 0. zero. zilch. nada. money gone.

40% will return 1-3x and will get you to break even.

10% will go to 10x and drive all your returns.

Within that, you may have the rare company that goes to 100x, 1000x, or more.

Distribution on returns across a diverse angel portfolio

Angel investing doesn’t work on a standard bell curve of average returns. With startups, the big wins are so big that they more than make up for the losses. It’s called the power law.

This is why (portfolio) size matters.

If you pick only one or two companies, statistically, they will likely go to zero. The more companies in your portfolio, the more likely you are to get one that is an outlier. And that outlier will dwarf all the failures. The reason to build a diversified portfolio is to maximize the chance of having a few big winners in the bunch.

Pro tip: The power law only applies to tech-scalable type companies. CPG investing has a different return profile. We’ll talk about that more later.

The J Curve

Startups that are going to fail typically do so within the first 3-5 years. Successful startup investments usually take 7-12 years to deliver the cold, hard cash return of a liquidity event. That means your angel portfolio returns over time will look like this - a J Curve.

A generic J-curve image we found on the internet - you get the point.

Isn’t that a screw? Just when you start to settle into your angel style, you start getting bad news. Your first investments may begin to fail, and it feels cruddy.

Pro tip: We’ll talk about how to be a great angel later. But for now, remember, as cruddy as it feels to have an investment fail, it feels worse for the founder.

Exit Events

Traditional startup exit events include shutdowns, acquisitions, and IPOs. As companies stay private longer, secondary sales are becoming more common. Secondary sales are when early investors sell some or all of their ownership to later-stage investors. For example, Series B or C investors actively seek to buy out smaller early-stage investors or SPVs.

If you invest in a venture fund, the fund manager decides whether to “take some money off the table” at an earlier round. The same is true for an SPV if it is actively managed. We’ll talk more about this later.

The Wrap Up

Angel investing is a loooong game. The daily dopamine hits don’t come from markups. They come from following a founder on their journey and from the new learning and new people you meet along the way.

So budget and invest to keep the learning fresh while you wait for those returns.

More questions? Leave a comment. Click on the green diamond to chat. Or drop into a new member welcome session on Fridays. Sign up here.

Fab Resources on Angel Returns

If you want a real-life example, here is a breakdown of Loom’s recent acquisition and how investors fared. https://growthmind.substack.com/p/assessing-loom-investor-performance

Halle Tecco has a great two-part series reviewing her angel investing results over the past 10 years. https://www.halletecco.com/blog/angel-investing-part-1

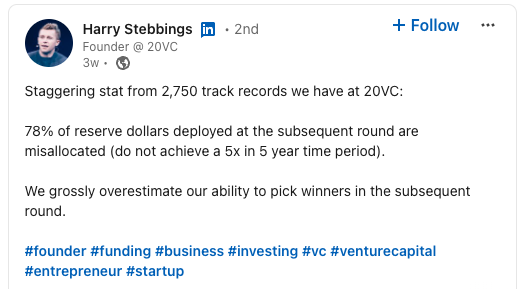

Harry Stebbings has seen a lot, so when he shares an insight, take notice. My favorites: